LIB.V Part 2: Catalysts, Competition, and the Decision Thesis

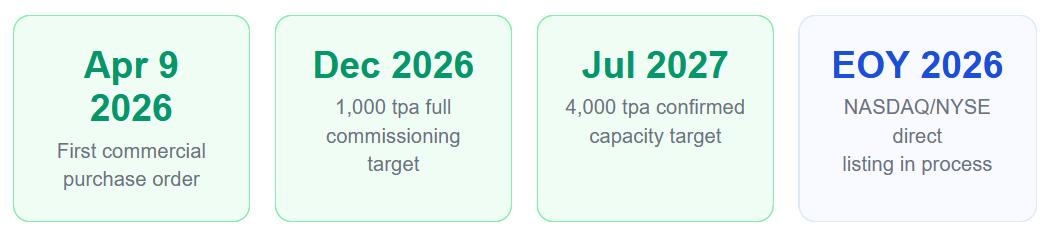

Commercial production started April 9, 2026. A NASDAQ listing is in progress. No North American competitor is producing from oilfield brine. Here's the full analytical picture.

From Part 1

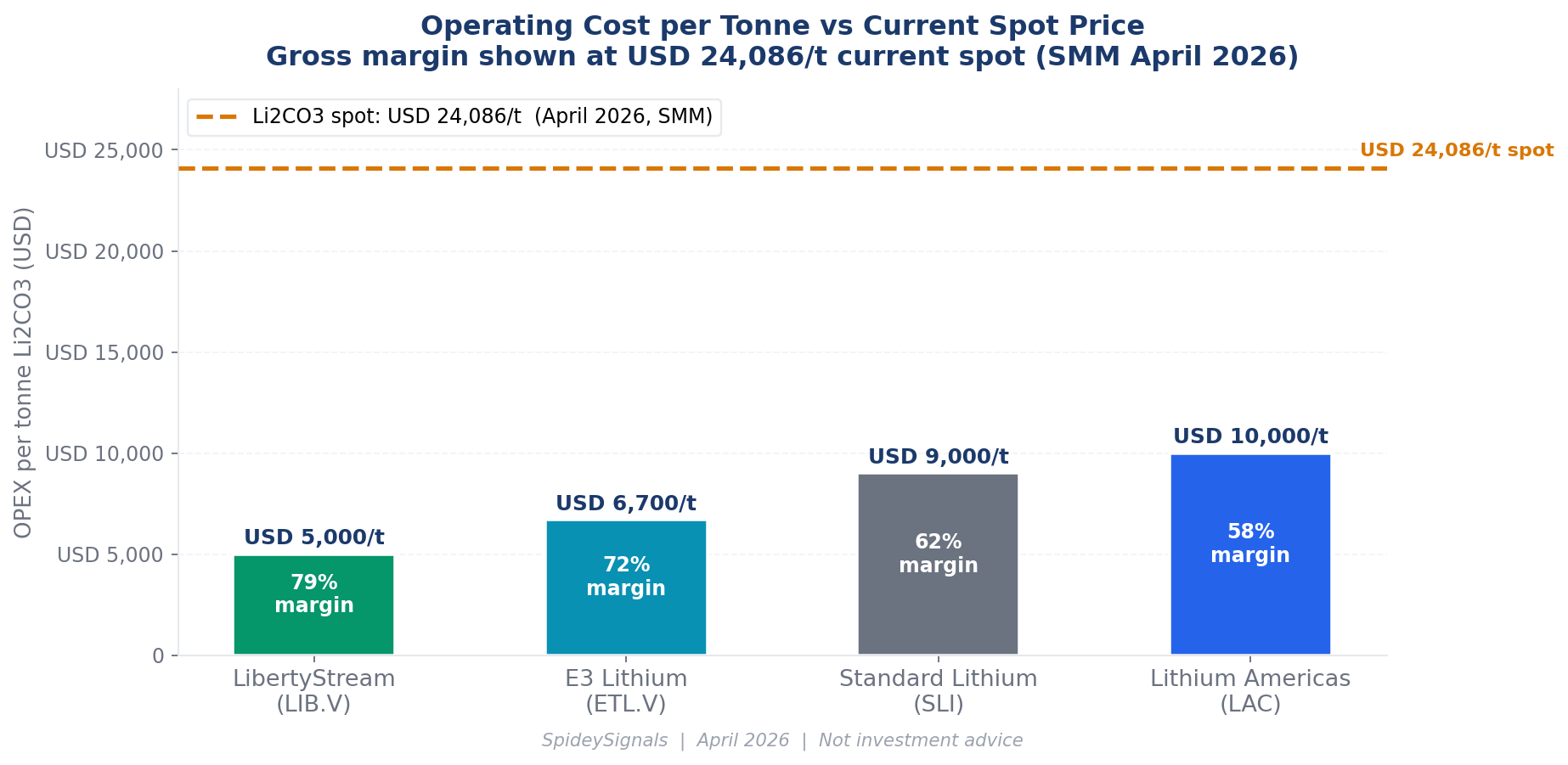

LibertyStream (TSXV: LIB) extracts battery-grade Li₂CO₃ from Permian Basin and Bakken oilfield produced water using a proprietary TiO₂ nanotechnology sorbent — the only commercially deployed DLE solution designed for 25–55 mg/L North American brine. OPEX ~$5K/tonne (audit-certified). Gross margin 79% at today’s $24K spot. $20M per 1,000 tpa module. 152× more field data than the nearest peer. Feedstock is a free waste stream.

On April 9, 2026, LibertyStream received its first commercial purchase order for battery-grade lithium carbonate(Only 1 tonne but part of Broader offtake agreement conversations link). The company crossed from technology story to revenue story. Now the question is what happens next — and whether the current market cap reflects what’s coming.

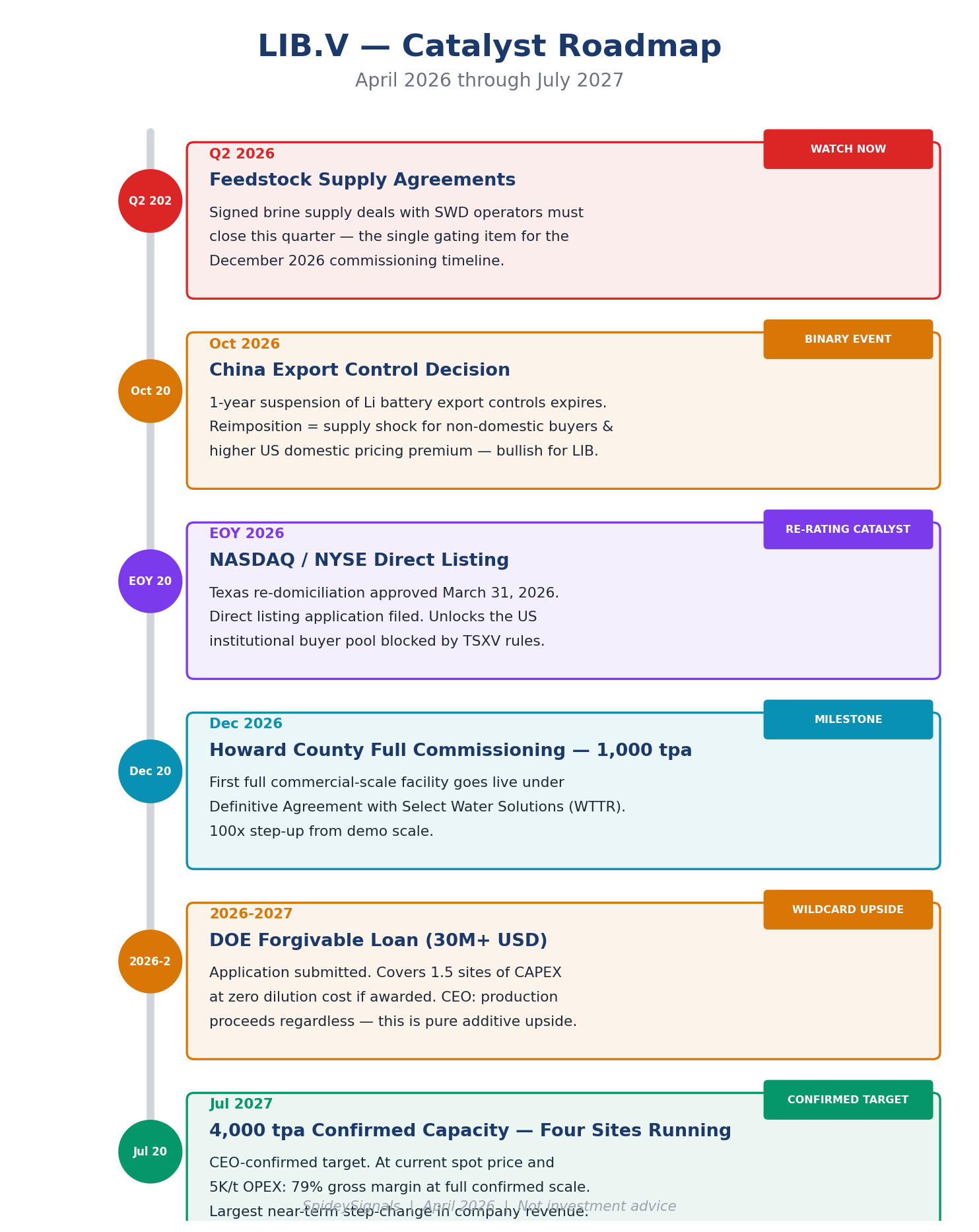

The Catalyst Stack — What’s Coming and When

Here are the catalysts I’m tracking in order of timing. Each one is a potential step-change in how the market prices this company.

The NASDAQ Listing — Why This Is a Bigger Deal Than It Sounds

What Uplisting to a US Senior Exchange Actually Means

LibertyStream currently trades on the TSX Venture Exchange. This matters more than most retail investors realise. A large portion of US institutional capital — mutual funds, ETFs, pension funds, family offices — literally cannot hold TSXV-listed securities under their investment mandate restrictions. It is not that they choose not to. Their investment policy statements often prohibit it. Venture exchange listings in Canada carry regulatory designations that exclude much of the US institutional buyer pool entirely.

LibertyStream is not pursuing an OTC upgrade, which would still leave it in a grey zone for many funds. They are applying for a direct listing on NYSE or NASDAQ — a full senior US exchange application. The Texas re-domiciliation was the legal prerequisite, approved by shareholders on March 31, 2026. The listing application is active. Expected timeline: end of 2026 or early 2027.

When this happens, a new pool of institutional capital gains the ability to buy the stock for the first time. Comparable Canadian resource and technology companies that uplisted to US senior exchanges have seen meaningful re-ratings, often within weeks of the effective listing date. The NASDAQ catalyst is not priced in. It cannot be priced in until the listing is complete.

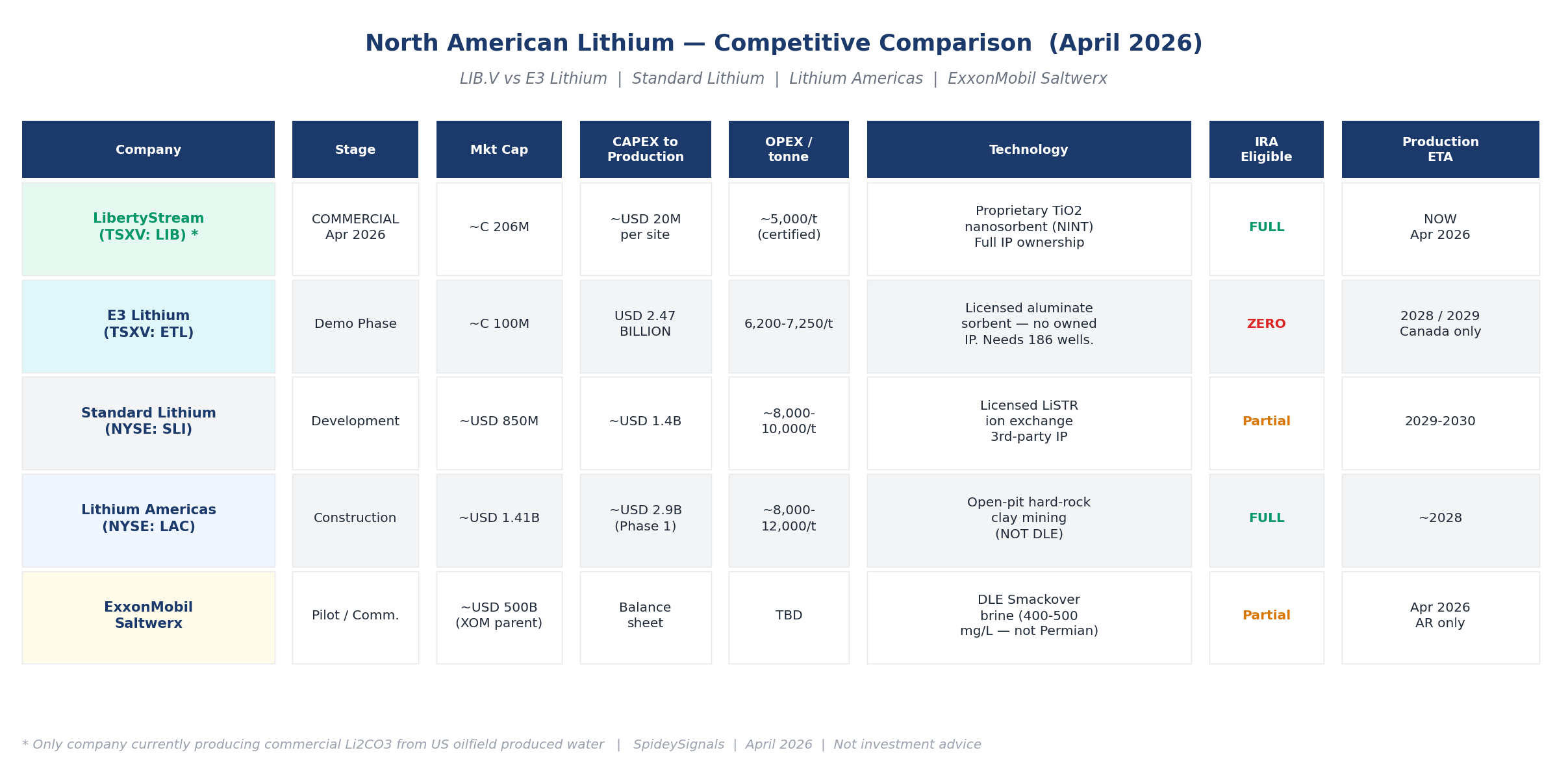

The Competition — A Full North American DLE Comparison

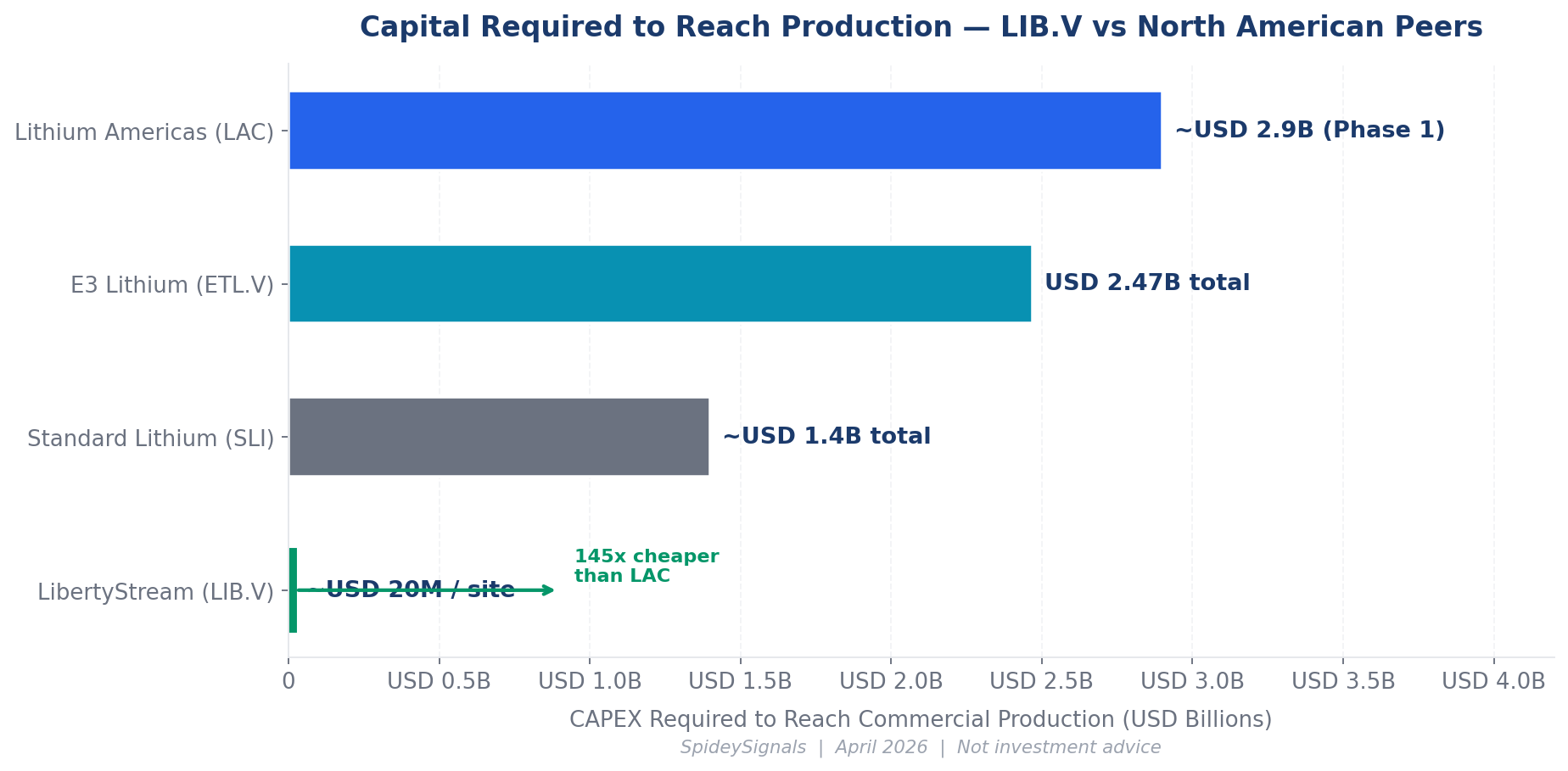

This is the section that requires the most analytical honesty. LIB gets compared to several companies by retail investors. Here’s the full picture across every meaningful North American DLE and lithium competitor.

North American Lithium — Full Competitive Comparison (April 2026)

Key Competitor Notes

E3 Lithium vs LIB: E3 has compelling PFS economics ($3.72B after-tax NPV, 24.6% IRR) but needs to finance $2.47 billion — more than 25× its current market cap — before producing a single commercial tonne. And its Alberta location means zero access to the IRA domestic supply premium that is central to LIB’s business case. E3 and LIB are not really competing for the same market.

Standard Lithium vs LIB: SLI trades at ~$850M pre-revenue with a 2029–2030 production timeline, backed by Equinor (45%). Their Arkansas Smackover brine runs at 200–400 mg/L — a completely different operating environment from LIB’s 25–55 mg/L Permian brine. Their licensed LiSTR technology would not work in LIB’s operating environment. Same macro thesis — US domestic lithium, IRA tailwind, DLE technology — completely different risk/return profile. The market is pricing SLI at 4× LIB’s market cap for production that is 3–4 years away.

Lithium Americas vs LIB: LAC is building a conventional open-pit hard-rock lithium mine in Nevada. $2.9B CAPEX, DOE loan commitment, GM equity backing. It’s not a DLE company and not really a peer for LIB. When built, it will produce significant volume — but it’s a fundamentally different business model, different risk profile, and the open-pit environmental opposition in Nevada has created years of permitting delays already.

ExxonMobil Saltwerx: XOM’s Saltwerx commenced commercial production from Arkansas Smackover brine (400–500 mg/L lithium) in April 2026 — the same week as LIB. The critical point: Smackover brine at 400–500 mg/L is approximately 10–15× more concentrated than Permian produced water. XOM’s technology works on Smackover. If XOM tried to enter the Permian, it would need to develop different technology for 25–55 mg/L brine, then build new SWD operator relationships from scratch against LIB’s existing network. XOM’s balance sheet is unlimited — this is a long-term watch item — but the near-term threat to LIB’s Permian franchise is low.

The Risks — Unsanitised

What Could Go Wrong

MED -Feedstock deals this quarter. Signed brine supply agreements with SWD operators must happen Q2 2026 for the December commissioning to stay on track. No announcement by end of June is a yellow flag. This is the #1 watch item.

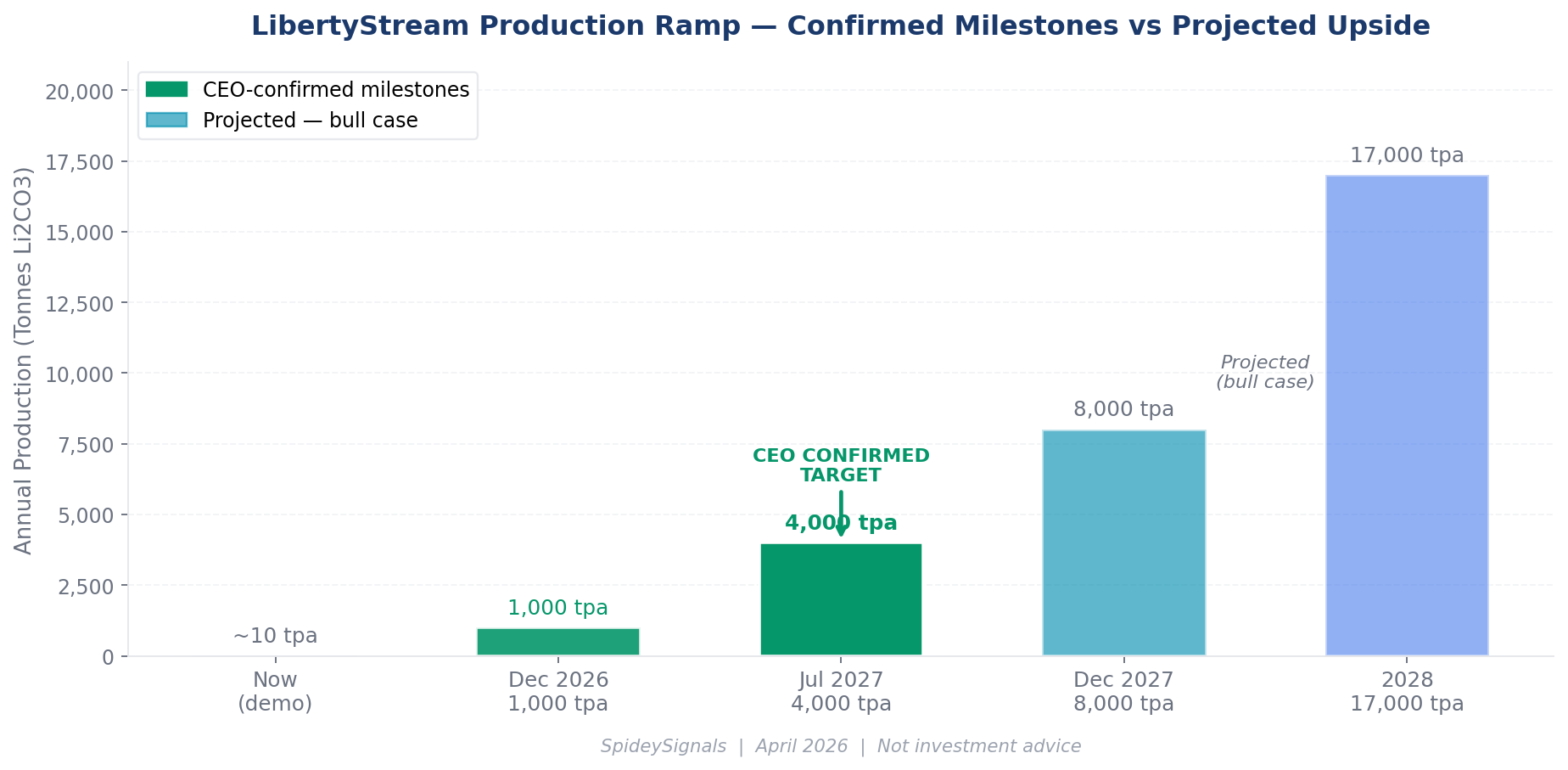

MED - 100× scale-up — first commercial build. The Howard County facility is the first commercial-spec module of its kind. Demonstration scale was ~10 tpa. Commercial is 1,000 tpa. The modular design reduces engineering risk versus a mega-plant, but the first build at full commercial spec is still an unproven step. Technical problems = timeline slips.

LOW- Dilution is structural. Three more sites = ~$60M CAPEX. Even with a DOE loan covering part of it, equity will be issued. Base-case dilution through July 2027 is approximately 9% (212M → 232M shares) — manageable but real. Good Dilution for Ramup is good news for the Market

LOW- Goldman Sachs is bearish on lithium. Their published 2027 forecast is $9,250/tonne — less than 40% of today’s spot. Goldman’s 2026 forecast was $8,900; actual is $24,086. They’ve been materially wrong. But Goldman has a $150B research department and they’re not dismissible. At $9.25K spot, LIB is still EBITDA-positive at $4,250/t margin — the business doesn’t break, the growth story slows.

MED - ExxonMobil long-term. XOM’s balance sheet is unlimited. If they decide the Permian oilfield brine DLE market is worth entering — new technology, new SWD relationships, 2–3 year runway — they could. This is a long-term risk to monitor in 2028, not a near-term threat.

The Decision Thesis — Why I’m Bullish

I said at the start I’d give you an analytical basis for a decision. Here’s mine.

The Bull Case — In Plain Terms

✓ They’re producing now. April 9, 2026 — first purchase order. The “will the technology work?” risk that defined the 2024 lows is permanently off the table. The question is purely execution from here.

✓ The economics work at today’s price — not a forecast. $24,086/t selling price. $5,000/t OPEX. 79% gross margin. Today. No lithium price appreciation required for the business model to make sense.

✓ The July 2027 milestone is confirmed, not projected. 4,000 tpa confirmed by management and institutional shareholders, all we need is to get the offtake agreement signed and 1000 TPA unit online. At current spot pricing, this milestone generates substantial annual revenue with industry-leading margins. The market currently prices in zero credit beyond December 2026.

✓ The domestic supply premium is structural, not cyclical. IRA Section 45X, DoD domestic procurement mandates, and Project Vault ($12B US government critical minerals reserve) create a buyer class paying a premium for US-produced lithium that exists regardless of global spot price moves.

✓ NASDAQ listing unlocks new institutional buyers. Legal groundwork done. Application active. When it happens — EOY 2026 or early 2027 — a pool of US institutional capital that currently cannot hold this stock gains access. This is a genuine re-rating catalyst with no precedent in LIB’s current price.

✓ No North American competitor is producing from oilfield brine. E3 is 2+ years away and needs $2.47B. Standard Lithium is 3–4 years away and needs $1.4B. The production lead is not closing — it is widening.

✓ Unmodelled upside is real. By-products (boron, rubidium, magnesium), the $30M+ DOE forgivable loan, the Barnett Shale as a third basin, and strategic offtake deals with gigafactory operators — none of this is in the base case. Any of them materialising is additive.

✓ The downside floor is much higher than 2024. The 52-week low was C$0.165 when zero-production risk was real. That risk is eliminated. The floor is validated IP, active contracts with NYSE-listed counterparties, government grants, and a partner with skin in the game. The asymmetry looks structurally different from where it stood 18 months ago.

None of this means the stock can’t go down in the short term. Small caps are volatile. The feedstock deal timeline is real. Lithium prices can move. I’m not telling you what to do with your money. I’m sharing why I find the risk/reward here — with the confirmed milestones, the NASDAQ catalyst, the 9% dilution math, and the production lead over every named competitor — unusually interesting.

Do your own work. Read the filings. Understand the risks. Then decide.

— SpideySignals https://x.com/Spideysignals